|

|

|

|

| REAL ESTATE |

|

|

|

Lifeline not enough

Lifeline not enough

Union Budget for 2013-14 has been a mixed bag for the real estate industry with the optimism on sops for first-time home loan buyers being dented by the imposition of 1 per cent tax deduction at source for sale of property beyond Rs 50 lakh.

The home for two

Green house

tax tips ● How can I claim rebate on rental income? ● Can co-borrowers claim exemption on home loan EMIs? ● Can I claim rebate on second home loan?

REALTY GUIDE ● Builder has backed out on promises ● How can I leave property for my devoted son? ● How can I get a clear title?

|

|

|

|

Lifeline not enough

Union Budget for 2013-14 has been a mixed bag for the real estate industry with the optimism on sops for first-time home loan buyers being dented by the imposition of 1 per cent tax deduction at source for sale of property beyond Rs 50 lakh.

However, the mood in the sector is largely that of disappointment as several demands of the sector have not been met.

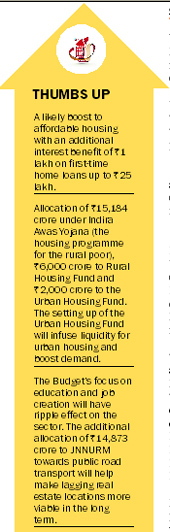

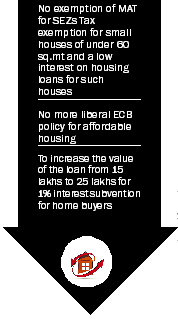

No silver lining Realty developers apex body CREDAI expressed disappointment over the Finance Minister missing out on affordable and rental housing and banking reforms. CREDAI, however, praised the Finance Minister for accepting the suggestion for home loan interest incentives for sub-Rs 25 lakh buyers, but, honestly we were expecting a lot more, said Lalit Kumar Jain, National President CREDAI & CMD Kumar Urban Development Ltd (KUL). Jain said the first-time home loan borrowers of properties of sub-Rs25 lakh will be allowed an additional deduction of Rs 1 lakh. However, the caveat on this sop is that buying a home is a big-ticket decision which is primarily based on future expectations, growth in jobs and income. Given the huge slowdown in the economy with the latest GDP numbers coming in at 4.5 per cent, growth, jobs and incomes are all in serious doubt. Historically, it has been seen that home purchases have been made even in a high-interest rate regime and tax sops or interest rates are lesser factors in a home buyers decision. The pre-dominant factor is whether he/she feels that he has a steady job and incomes will grow in the future. Smaller centres to benefit from tax sop The benefit of this sop may be felt more in the smaller cities where the ticket size of a home is smaller as compared to that in bigger cities. Tanuj Goel, Executive Director, KDP Infrastructure says, The Budget seems to have given some hope to the real estate segment though the real expectations remained unfulfilled. Goel says this provision is only for the first year and with a carry-forward benefit of the unutilised deduction to the second year. This will help boost housing sales in tier II and III cities, peripheral areas and distant metro suburbs, but not within the metropolitan cities. Sanjeev Srivastva, Managing Director Assotech Limited echoes the same sentiment by maintaining that the additional deduction of interest up to Rs 1 lakh is a good move to encourage new buyers to think of buying a home. This is going to increase affordable home market and may give boost to affordable housing projects. Multiplier effect may bring some solace This can also have a multiplier effect for related industries. Gagan Banga, CEO of Indiabulls Financial Services says it will not only help housing as such, but will also lead to an increase in demand for steel, glass, cement and several other industries. Among the beneficiaries of a growth in real estate demand could be the air conditioner manufacturers. Kanwal Jeet Jawa, Managing Director, Daikin India , says by stressing on one of the most critical components of the Indian economy the real estate sector, the Finance Minister has opened the doors for greater bloom in the Indian HVAC market as well. With a direct correlation between the two sectors wherein growth of the real estate sector supplements the growth of the HVAC sector, factors like issuance of an additional deduction of Rs 1 lakh for people taking a home loan on their first home during the period 2013-14, shall help investors invest more in real estate which will thus augment the reach of the HVAC industry as well. The bitter-sweet TDS pill The real estate industry, however, is peeved at the Budget provision of levying TDS at 1 per cent on sale of property above Rs 50 lakh , which, they fear, may hurt demand. According to R.K Arora, Chairman and Managing Director, Supertech Limited, The real estate industry which has been looking to the annual budget for relief, is highly disappointed with the decision to levy TDS on property transactions beyond Rs 50 lakh. This decision is likely to create a recession in a market already facing a slump, he added. The idea is to get more transactions under the tax net. Says Pankaj Bajaj, President CREDAI NCR & MD Eldeco Infrastructure on the high value transaction tax, the idea behind 1 per cent TDS on property transactions of more than Rs 50 lakh is clearly to bring more and more property transactions under the tax ambit especially in the re-sale market where a significant component of the transaction value tends to be in black. This provision will also curb speculation in the property market. Goel says , TDS of 1 per cent to be charged on the transfer of immovable property shall curb speculation and bring about improved reporting and accountability in high-value immovable property transactions. Considering that the TDS is to be charged on the gross transaction value rather than net gains, sellers will have a cash-flow impact in situations where the sales are at a loss or at zero/negligible gains. Expensive luxury However, luxury properties will become even more expensive due to changes in service tax rules. Goel adds that the rate of abatement on homes and flats of above 2,000 sq ft or costing Rs 1 crore and above has been reduced from 75 to 70 per cent. Effectively, this translates into an increase in service tax outflow, which means that luxury housing will now become even more expensive. Fringe benefits The real estate industry will benefit from increase in outlays of government schemes. Suresh Gogia, CMD, Ascent Buildtech says the proposed raise in allocation to the Rural Housing Fund from Rs 4,000 crore to Rs 6,000 crore also cant be ignored as a motivator. Goel adds that the additional allocation of Rs 14,873 crores to JNNURM towards public road transport will help make lagging real estate locations more viable over the longer term. An urban housing fund for Rs 2,000 crore has also been announced in the Budget. Industry reacts The sector feels disappointed for not getting infrastructure status and the imposition of 1 per cent TDS on property worth more than Rs 50 lakh will create an impact on the overall growth of the real estate

industry. There were no announcements to grant an industry status to the sector and no clarity is there on the continuation of interest subvention of 1 per cent on home loans for affordable

housing. Rajendra Kumar Panpalia, MD, Wave Group The real estate sector is constrained in supply, and none of the items: granting an industry status, infrastructure status for township projects or FDI rules have been mentioned. Affordable housing supply will remain constrained because of this. Luxury houses will also cost more due to decrease in the rate of abatement. Overall a do not rock the boat

Budget. Vineet Singh, Business Head, 99acres.com Indian real estate will continue to struggle with its larger hurdles. While the affordable housing category has been rightly given due attention, aspects relating to improved transparency and corporate governance within the sector have been largely

ignored. Anuj Puri, Chairman & Country Head, Jones Lang LaSalle

India I hope that measures proposed in the Budget aimed at promoting infrastructure growth, reforms in the financial sector and industrial development will be implemented effectively, in order to propel India towards a high growth

trajectory. Anshuman Magazine, CMD, CBRE South Asia Pvt Ltd. This was a reasonably encouraging Budget in general, but unenthusiastic for the Indian real estate

sector. Sanyam Dudeja, COO Punjab, Taneja Developers & Infrastructure Ltd. High interest rates and soaring land prices have been the major resistance factors in reviving the demand for housing stock and the Budget could have announced a few long-term steps aimed at improving the supply of land and reducing interest

rates. David Walker, Executive Director, SARE Homes

Sore points Input costs like those of marble have gone up. Arora says raising the excise duty on marble from 30 to 60 per cent is also likely to affect the cost of housing. He adds that the effect of increasing the income tax exemption from Rs 2 lakh to Rs 2.20 lakh is marginal and not sufficient to increase the purchasing power of taxpayers. The proposal to raise surcharge from 5 to 10 per cent for companies earning profit beyond Rs 10 crore is highly discouraging and is penal in nature, he adds. The disappointment in the industry is more on account of several demands that have not been met. Jain of CREDAI says the developer community is thoroughly disappointed that the Finance Minister has not given any directions to the RBI on the imperative to support real estate funding. Arora laments that none of the suggestions of real estate industry like giving industry status to real estate, allowing benefit U/s 80 IB to developers to promote affordable housing or reduction of excise duty on cement or steel have been considered in the budget proposals.

|

||

|

With the wedding season on a number of new couples are on the threshold of setting up a new home. The trend of nuclear families also sees young couples embarking on a journey to create their dream abode. What does it really take to make a home for two? The aim is to make a statement that is both striking and subtle.

Before deciding about the furniture, one must think of the existing space and possibilities of its enlargement physical as well as visual, comfort and practicality, the language of design, interior planned/ existing, introduction of colour. It is important to be aware of the available choices before zeroing down. Choices can be made out of the following: ●

An understated interior with a bold furniture presence. ●

A dressy interior with subtle furniture. ●

A simple, elegant interior with minimalist or straight lined furniture. ●

Having decided on the design language, materials and finishes need to be worked upon: ●

Wood and steel combinations which give a warm, high tech feel. ●

Rich plush finishes with leather overtones. ●

Cold materials like steel and glass punctuated with warm colours. ●

Last but not the least, a deliberate fusion look, simple modern designs coupled with opulence. In India wedding is looked at as a big festival, there is a lot of coming and going and everybody has to see the couples room or home, as the case may be. It is the first glance that takes in the complete décor and the ambience. The writer is an Interior Designer, IM Center for Applied Arts Trendy tips ●

Use monotone finishes on the walls and go for a warm medium to dark-toned wooden floors without any patterns. A self-textured ceiling with cove lighting also adds elegance to the room. ●

Mood lighting plays a significant role. You can control the intensity of the lights too. Go for bright lights when you are hosting a party, lamps and niche lights when its just the two of you. Colour-changing lights are glamorous as well as romantic. ●

For upholstery, opt for neutral fabrics with bold patterns. Play with a combination of black and white or chocolate or turquoise. ●

Add throws in brocade or with leather trimmings. Bright cushions could be the highlight of your bed linen. Your headboard could be leather on leather or wood-draped leather. ●

Wardrobes within the bedroom is not advisable. But if you still want to go for it then these need to be cleverly camouflaged by a screen which in itself could be highlight of the room. Otherwise, opt for a walk-in closet. ●

Make sure you buy a full-size mirror and a dressing drawer for your beloved. ●

Whatever be the line of thought, it should be borne in mind that it is not just the main line furniture but the odd man out that would stand you apart.

|

||

|

Steps to save your prized plants

C.S. BEWLI ... All plant lovers must have lost their precious plants at one time or the other. Sometimes one tends to lose good plants in spite of taking all precautions. However, in a majority of such cases water is the main cause for losing plants. It is important to have adequate knowledge of some useful techniques to ensure the survival of your prized possessions.

Plants need a continual source of moisture in their roots to allow the distribution of vital nutrients throughout their structure. The plants will not survive if there is malfunctioning in this system. Damaging factors Normally bonsais and other potted plants die due to root damage due to over or under-watering. Over-watering causes water-logging of roots which is reflected by ●

The foliage of the plant turns yellow during the peak growing season. The leaves eventually drop and the plant looks wilted. ●

The presence of wet root system reduces the ability of compost to absorb air as over-watering fills the needed oxygen spaces in soil. This affects the root hairs which are much more efficient than the larger thick roots at absorbing water and other nutrients from the soil. ●

If no remedial action is taken immediately, with the passage of time decaying of roots continues and soon roots are unable to support the growth of the plant and die eventually. ●

On removing the root ball from the pot the compost will smell foul and rotten; the root tips turn black with no signs of fresh growth of roots. Under-watering causes desiccation of roots which is reflected by ●

The leaves and branch tips shrivel and become dry even in the growing season due to the non-availability of moisture at the roots and inability to absorb nutrients from the soil. ●

The leaves tend to droop. ● On removing the root ball from the pot the roots will appear desiccated without any sign of their being swollen or inflated and resemble dry and twisted twines. Remedy Sphagnum moss plays a very important role in reviving sick plants due to its excellent water retention ability coupled with its fast draining property. It is an excellent growing medium for plants with weak roots, as it keeps the roots well aerated and helps in promoting root development. This golden property of sphagnum moss is utilised at the time of propagation of plants by means of air layering to develop fresh roots. The moss used should be cleaned of weed, grass or any other extraneous material. On identifying the above symptoms of the sick plant, the following remedial action should be taken immediately: ●

Take out the root ball from the pot to stop any further root rot. Carefully remove the compost and cut off all dead and rotten roots without damaging any live roots; rotten soil should be sprayed with water for its removal. ●

A suitable deep pot is taken and a layer of clean and moist sphagnum is placed in it. Position the sick tree at the centre and keep adding sphagnum around the roots of the plant while working with your fingers till it reaches the brim of the pot. ●

Spray the moss with water to keep it moist and cover the plant with a clean and fresh transparent plastic bag. Place the plant in shade. ●

Check the plant the next day; it should have slight moisture around the plastic bag. If too much moisture condenses on the sides, the top of the bag should be opened for a few hours. ●

The plant, while in plastic bag will function in its own self-created micro environment. ●

New roots will sprout within three to four weeks. During spring, remove some moss from the top and add cactus compost. Remove the polythene bag and allow the plant to grow like this for about a year, before next re-potting. ●

Even if about 40 per cent of the roots are alive, there are bright chances of the plants revival. ●

For the success of this operation, the moss should be kept moist and not soggy.

|

||

|

tax tips Spouse issues on ownership Q.Kindly refer to your answer in The Tribune Real Estate (dated February 16) with heading House in wifes name. My query is that after purchase whose property will this house be i.e. of the wife or husband? Also rental income, if any, of this house will be considered wifes income or that of the husband for the purpose of income tax. Additionally, if the husband purchases a house in the name of both without capital gain income, what will be the status? Vijay It may also be added that under the provisions of Section 64 of the Income-tax Act, 1961 (The Act), the income arising from asset transferred directly or indirectly to the spouse by an individual other than for adequate consideration or in connection with an agreement to live apart is taxable as the income of such individual. In the case in reference, funds have been provided by you for purchasing a house property in the name of your wife. Therefore, income arising from such house property shall be taxable in your hands. How can I claim rebate on rental income? Q.I have taken loan for house which is self-occupied and interest is more than Rs 1.5 lakh. I want to claim rebate for rental income (more than Rs 1.5 lakh) of other house against which there is no loan. Can I claim rebate for more than Rs 1.5 lakh. Please clarify. Vijay Singal A.The deduction in respect of interest payable on the amount borrowed for construction of a house is allowable against the income from house property against which the amount has been borrowed. It would not be possible for you to claim the amount of interest which is in excess of Rs 1.5 lakh from income arising from the house property which has been let out but in respect of which the amount had not been borrowed. Can co-borrowers claim exemption on home loan EMIs? Q. On April 30, 2012 (registry date), we had purchased a 4BHK flat in Dera Bassi (Punjab) & the flat is in the name of my mother, myself and my brother having percentage share of 50, 25, 25, respectively.

Now, since my mother is a housewife and has no source of income, so I and my brother want to take all the tax benefits. Is it fine? Or do we need to divide it between the three of us and in what proportion? Can we divide it in whatever way we want? Is it possible that I take the interest benefit while my brother takes the principal benefit? Do we need to share it in a fixed ratio and can we change it in next financial year? Pre-EMI comes under Section-24B? Right? Pre-EMI of Rs 5,576 was deducted from my account for the period between April 30, 2012 and May 10, 2012 (the day of 1st EMI). Lastly, are "stamp duty", "service tax" exempted from income tax? If yes, then under which section? FYI - Total interest component for the year = 153231 + 5576 (Pre-EMI) Total Principal component = 25299

Varun Verma

A. Your queries are replied hereunder: ●

A deduction in respect of repayment of principal amount will have to be in the same ratio in which the amount was borrowed. Accordingly, you and your brother would be entitled to a deduction to the extent of 25 per cent of the repayment of principal amount. ●

The amount of deduction allowable in respect of interest paid / payable on amount borrowed for purchasing or constructing a house is allowable under Section 24(b) of the Income-tax Act 1961. The deduction would be allowable in the same ratio as stated above. In case of a self-occupied property, the allowable deduction is limited to Rs 1,50,000 only. ●

Stamp duty and registration charges are allowable as deduction under Section 80C of the Act within the overall limit of Rs 1,00,000. The deduction in respect thereof would also be in the ratio in which the house is owned by the three co-owners.

Can I claim rebate on second home loan? Q.We are claiming house loan benefit in our IT return on the house which is occupied by us and we are also paying house loan on second property which is a flat in New Delhi. Can we take benefit on this house loan also which has not been let out or is occupied by anybody? Rajesh K. Grover Deduction allowable under Section 80C of the Act in respect of repayment of amount borrowed for the purposes of purchase or construction for both houses shall have to be within the overall limit of Rs 1,00,000. The allowability of deduction of interest paid/payable on the amount borrowed for purchase or construction of a residential house is restricted to Rs 1,50,000 in respect of self-occupied property. In case both the houses are self-occupied, deduction allowable would be restricted to Rs 1,50,000 only. In case it is not self-occupied but is intended to be let out, deduction for interest paid/payable would be allowable against the annual value to be computed in accordance with Section 23(1)(a) of the Act. The annual value will thus be computed at a sum for which the property might reasonably be expected to be rented out from year to year.

|

||

|

REALTY GUIDE Q. I have booked an apartment in Amritsar and have paid two instalments of 10 per cent of the total cost. The builder had assured me that he would help me arrange the balance amount from some leading banks with which they had a tie up. But that builder has sold the entire project to a new company and the new company is unable to show any tie-up with any financial institution due to the lack of approvals from the city corporation.

Apart from this, the new company has changed the floor plans of my apartment without any prior information. The first builder has issued me the allotment letter but I was never issued any letter regarding the sale of the project or change in plans. As the cost of construction has increased, the new builder is also using substandard materials to cover his costs. Please advise me what should I do and let me know which authorities can be approached to file the complaint against these builders.

K.K. Saini A.your query it is clear that you did not investigate properly before making the investment and have committed a mistake. You have not checked the credibility and background of builder and had not verified his track record. From your query it is clear that you have invested in an unapproved project. You hav, however, not mentioned whether you have signed any agreement with the builder or not. You have written that the builder had promised to help you get the finance from some leading banks. But verbal agreement has no meaning until you have any proof. Take the services of some advocate to get some relief by filing your case in consumer court. How can I leave property for my devoted son? Q.I am 80 years old and have four sons. Three of my sons are well settled in a big city and have good jobs. The youngest one, however, is living with me in a village. I have 8 acres of agricultural land, out of which 2 acres are inherited by me from my parents and six acres are self-acquired. My youngest son has been taking care of me, while my other sons have had no contact with me for the past 26 years. They have given me no emotional or financial support all these years. Now, I don't want to give them any part of my property and leave the entire property to my youngest son. I have been advised to make a Will. But I have no knowledge of such issues. Please suggest how I can leave my all property to my youngest son, so that my elder sons cant claim it after my death. Shriniwas Rai A.You can handle this matter in two phases: ●

You have full right to leave the six acres of your self-acquired agricultural land to your youngest son. But, I will advise you not to make a Will because your other sons will create a problem for your younger son after your death. It is better to make a gift deed and change the ownership of this property in revenue records in the name of your youngest son during your lifetime. By this he can become an undisputed owner of this property. After your death your youngest son will enjoy the property with clear and transparent title. ●As for the two acres inherited by you it will be better to make a Will for that in favour of your youngest son to the extent of your share only. Q.A commercial plot was purchased in 1990 and registry was done in tehsil office. But, intekal has not been executed till date. Now the patwari has informed that the share of the plot is not registered in his books (in other words, the previous owner re-sold the plot without an intimation to the registered owner. What is the remedy in the absence of intekal which according to the patwari is a must ? Tarsem Singh A.You are a genuine (undisputed) owner having valid lawful possession of the plot. You should not worry as you have the title deed (registry) present and the previous one with you. You dont have only mutation with you. You should take the help of an advocate dealing in property matters and file a civil suit under the Transfer of Property Act, 1882. You should take a direction from the court and civil court will make a direction to the patwari do the intekal in your favour. By this, the title of your plot will become clear and transparent.

|

||

|

Azure business suites RPS Group has recently launched RPS Azure, a luxury executive business suites project. The new project is part of IT and Business Park RPS Infinia located on National Highway-2, Mathura Road, Faridabad. The group has already invested Rs 100 crore in the project. RPS Azure comprises 240 Executive Business Suites, with each unit, spread over 650 sq. ft of area. Speaking on the occasion Pradeep Seth, Group CEO, RPS Group said, With RPS Azure, we aim to set a new benchmark in the hospitality sector and provide an amalgamation of luxury, comfort and privacy. The units are priced at Rs 6,500 per sq ft and the construction would be completed by end of 2015. Kumar Urban Development Limited (KUL) has launched a mega township Kharadi and Hadpasar in Pune. With the project area of over 103 acres, the bookings for Phase-1 of KUL Nation will open this month. The project will have six high-rise buildings of 22 floors with 264 flats in each building - 12 flats of 1 BHK type with a carpet area of 35 sq m each flat. The second cluster consists of six buildings with 211 flats in each building, and 2 and 2.5 BHK-type flats with the carpet area ranging from 60 sq m onwards. The third cluster of the project includes 3BHK and 4BHK units of 120 sq m onwards. Announcing the launch, Ms. Kruti Kumar Jain, Director, KUL, said: "Kharadi is one of the rapidly growing localities in Pune. KUL Nation offers a unique combination of luxury and affordability, suited for all pockets. The prices range from Rs 20 lakh to Rs 60

lakh.

|

All plant lovers must have lost their precious plants at one time or the other. Sometimes one tends to lose good plants in spite of taking all precautions. However, in a majority of such cases water is the main cause for losing plants. It is important to have adequate knowledge of some useful techniques to ensure the survival of your prized possessions.

All plant lovers must have lost their precious plants at one time or the other. Sometimes one tends to lose good plants in spite of taking all precautions. However, in a majority of such cases water is the main cause for losing plants. It is important to have adequate knowledge of some useful techniques to ensure the survival of your prized possessions.

Bajaj said that what is disappointing is that the FM has not chosen to give any direct fillip to affordable or mass housing in the form of some kind of tax incentives. Any loss of revenue, in my opinion, would have been more than compensated by way of increase in construction activity as a result. Housing is a sector with maximum forward and backward linkages. Coupled with acute housing shortage, there was a real case for giving tax breaks for mass housing which has been ignored in this budget, he adds.

Bajaj said that what is disappointing is that the FM has not chosen to give any direct fillip to affordable or mass housing in the form of some kind of tax incentives. Any loss of revenue, in my opinion, would have been more than compensated by way of increase in construction activity as a result. Housing is a sector with maximum forward and backward linkages. Coupled with acute housing shortage, there was a real case for giving tax breaks for mass housing which has been ignored in this budget, he adds.

A.The taxability of income has to be ascertained with reference to the source of investment. In case funds belonging to husband are invested in an asset yielding income in the name of his wife, the income arising therefrom would be treated as income of the husband and would be taxable in his hands.

A.The taxability of income has to be ascertained with reference to the source of investment. In case funds belonging to husband are invested in an asset yielding income in the name of his wife, the income arising therefrom would be treated as income of the husband and would be taxable in his hands.  We had taken a loan of Rs 18.5 lakh from ICICI bank for the same. As per bank requirement, co-owners need to be co-borrowers in the loan. So, the loan is also in the name of my mother, myself and my brother. However, the EMI (17,853) is being deducted only from my account as I am the primary applicant.

We had taken a loan of Rs 18.5 lakh from ICICI bank for the same. As per bank requirement, co-owners need to be co-borrowers in the loan. So, the loan is also in the name of my mother, myself and my brother. However, the EMI (17,853) is being deducted only from my account as I am the primary applicant. A.The query does not indicate the nature of benefits being claimed. Reply to your query is based on the presumption that you have claimed deduction allowable under Section 80C and Section 24(b) of the Act.

A.The query does not indicate the nature of benefits being claimed. Reply to your query is based on the presumption that you have claimed deduction allowable under Section 80C and Section 24(b) of the Act. The new company is also pressurising me to change the apartment originally allotted to me because the construction of that tower may be delayed. As I have opted for a construction-linked payment plan, the company is warning me to opt for the tower where the construction has already started so that they can pressurise me to deposit more instalments otherwise my allotment would be cancelled.

The new company is also pressurising me to change the apartment originally allotted to me because the construction of that tower may be delayed. As I have opted for a construction-linked payment plan, the company is warning me to opt for the tower where the construction has already started so that they can pressurise me to deposit more instalments otherwise my allotment would be cancelled.