|

|

|

|

|

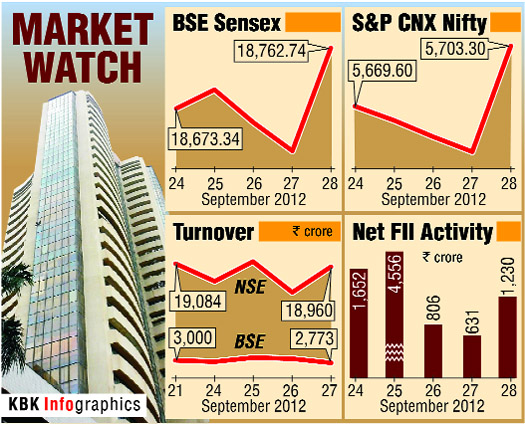

Markets to consolidate, may see profit-booking after recent rally

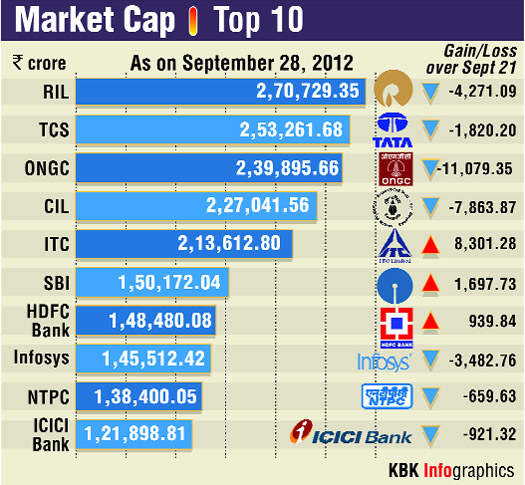

M-cap of top 7 firms dips by over

Rs 30k crore, ONGC hit hardest

Weak monsoon may push sugar output down to 24 mt this year

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

|

Panasonic plans to make India a manufacturing hub

Tax

Advice

personal

finance

Taking a home loan from a different city

|

|

Markets to consolidate, may see profit-booking after recent rally

Mumbai, September 30

Besides, investors will gradually turn focus on the second quarter corporate results that are to be announced from the second week, they said. "Markets will consolidate and move up in-line with further announcements on core reforms, which are now widely anticipated," Dipen Shah, head of private client group research at Kotak Securities, said. He added, however, "Any move from China to support its economy will be an added positive, particularly for commodities". This week, the stock market will remain closed on Tuesday, October 2. "The markets will also watch out for fiscal initiatives from the government and expectations are high on this front. The September inflation numbers will be more important as they will play a part in the RBI's rate decision in its next policy review meeting," Shah said. Besides, auto and cement shares will be in focus this week as companies from these two sectors will announce their monthly sales volume data for September. The BSE 30-stock benchmark Sensex ended marginally higher for the second consecutive week, touching 14-month high of 18,762 due to some buying towards the end of the week on the back of global rally triggered by Spain announcing a crisis budget for 2013. According to CNI Research chairman & MD Kishore Ostwal: "It seems the euphoria will slow down and some profit-booking is expected in a truncated week." Earlier this month, the government announced reform initiatives like opening up multibrand retail chains to foreign direct investment and allowing foreign carriers to pick up stake in domestic airlines. It also eased FDI norms for the broadcasting sector. Meanwhile, the government has said the rupee could touch the 50-mark to a dollar in the next four months on the back of strong inflow of foreign funds. "If rupee further strengthens, which we hope it will, with the steps the government is taking, we expect it could even touch 50 in the next 2-3 months or four months," Department of Economic Affairs secretary Arvind Mayaram had said on Friday. The rupee on Friday rose to an over five-month high of 52.49 against the dollar on strong capital inflows and hopes of more policy reforms. The local currency ended the week at 52.85 a dollar. The appreciation of the rupee will help cut down the subsidy bill and cool down inflation, which stood at 7.55 per cent in August, he had said. PTI

|

||

|

M-cap of top 7 firms dips by over Rs 30k crore, ONGC hit hardest

Mumbai, September 30

ITC, State Bank of India and HDFC Bank, however, saw rise in their market capitalization, totalling Rs 10,552 crore, in an otherwise sluggish stock market where the 30-scrip Sensex saw a mild gain of 0.05% during the past week. The market cap of ONGC plunged Rs 11,080 crore to Rs 2,39,895 crore, while Coal India lost Rs 7,864 crore to Rs 2,27,041 crore. Reliance Industries saw its value plummet Rs 4,271 crore to Rs 2,70,716 crore; Infosys lost Rs 3,482 crore to Rs 1,45,510 crore and TCS value fell by Rs 1,820 crore to Rs 2,53,264 crore. Besides, ICICI Bank's m-cap slipped Rs 922 crore to Rs 1,21,899 crore and NTPC lost Rs 659 crore to Rs 1,38,400 crore. On the other hand, FMCG major ITC's value surged Rs 8,040 crore to Rs 2,13,294 crore, while SBI added Rs 1,698 crore taking its m-cap to Rs 1,50,173 crore and HDFC Bank's market worth moved up by Rs 814 crore to Rs 1,48,258 crore. Of the top 10 companies, Reliance Industries was at the no 1 spot, followed by TCS, ONGC, Coal India, ITC, SBI, HDFC Bank, Infosys, NTPC and ICICI Bank. PTI

|

||

|

Weak monsoon may push sugar output down to 24 mt this year

Q: The Indian Sugar Mills Association has reduced its sugar production estimation by two million tonnes to 24 million tonnes for the 2012-13 crop season. Can you explain the reasons behind this projection?

Q: There is some confusion about sugar stocks in the country. How will you estimate the opening balance for 2012-13? A: Let us first look at the opening balance for the 2011-12 season. We now know that on an average, sugar mills sold nonlevy sugar from 2010-11 season's production till mid-December 2011, some had sugar till beginning of December, while others had stocks till end of December. Considering nonlevy consumption of 4 million tonnes up to mid-December, including festival demand of October, 2011, and levy sugar stocks of about 1.5 million tonnes of the past years, which were supplied up to May, 2012, the OB on October 1, 2011, was 5.5 million tonnes. With domestic consumption of 2.2 million tonnes (considering government releases) and exports of 3.5 million tonnes during 2011-12, and 2.62 million tonnes of production, the opening balance of sugar stocks for the 2012-13 season will be 6 million tonnes as on October 2012. Q: With lower sugar production next year and increase in sugar prices since July 2012, do you feel there is any need to import sugar? A: Import of any commodity should be and is generally resorted to when there is any shortage of the same within the country. Sugar should be no exception. As explained earlier, we will have a comfortable opening balance as on October 1, 2012, of 6 million tonnes, enough to meet the domestic requirement for over three months. Sugar production next year will be more than the domestic requirement. Therefore, it is absolute certain that there would be enough sugar to meet the country's needs. In fact, there may be a surplus too which could be exported. Imported sugar will only add to the surplus sugar stocks and with an unviable international market, opportunities to export are limited. Hence, the extra sugar so imported will only burden the domestic market and push prices down leading to cane price arrears. It could be harmful for the mills and the farmers. Sugar prices have to remain viable for the mills to pay remunerative cane price on time to farmers, so that they continue to remain interested in sugarcane in the 2013-14 season. Therefore, there should not be any big hurry to import sugar. Q: Considering your expectations about sugar production in the 2012-13 and season the global scenario, how do you see sugar prices next year? A: Experts in the field, estimate a global surplus of 6 to7 million tonnes in 2012-13. With good sugar production in Brazil, Thailand, India, Australia and the European Union, most of them would be looking to export sugar. On the other hand, China and Russia expect a better crop, which will reduce their import demand. Most traders and analysts are therefore, generally bearish on the international prices. However, with a good sugar production, adequately covering the domestic requirement, and throwing up a small, manageable surplus, the current sugar prices of around Rs 3,500-3,600 per quintal ex-mill should continue to prevail for most part of the next sugar season. Q: The government had announced a mandatory 5 per cent ethanol blending with petrol programme in 2007. With objections from one particular sector, it is not coming out with its pricing policy yet, how do you see this bio-fuel programme shaping up? A: The government's delay to finalize its ethanol pricing policy is harming the blending programme. This is despite the government's decision to implement the 5 per cent mandatory ethanol blending programme and procurement at a fixed price, has time and again, been reiterated by the Group of Ministers and the cabinet. The government has even fixed a target of 20 per cent ethanol blending by 2017 under the national biofuels policy of 2009. We have been accordingly supplying ethanol at the provisional price of Rs 27 per litre ex-factory for the past two years, even when other molasses based products are fetching a higher price of Rs 34-35 per litre. Ethanol producers have been losing by supplying ethanol and are pretty discouraged over the delay and lack of clarity in the pricing matter. The petroleum ministry is yet to issue its gazette notification for the mandatory 5 per cent ethanol blending. I feel that the ethanol blending programme can succeed in India only if the final ethanol pricing policy is announced before start of new sugar season from October, 2012.

|

||

|

Panasonic plans to make India a manufacturing hub

New Delhi, September 30 The companys production in India will get a boost with the commissioning of the US $200 million facility in Jhajjar in Haryana by December this year. Well focus on India as a manufacturing base. We are seriously considering to start exports from India and at present studying various markets around the world that are suitable for products manufactured here, Panasonic India vice president and board member Yutaka Suzuki told PTI. Once the firm operationalizes and commissions the upcoming Jhajjar plant, it will consider expanding the reach of its products to other countries as well, he added. PTI |

||

|

Tax

Advice By S.C. Vasudeva Q: My wife and I have nominated each other as beneficiaries in all our bank and post office accounts. In case of death of either one of us, will the account funds be taxable for the nominee? Also, is the interest on infrastructure debentures taxfree? And, can I get tax rebate for the funds deposited in my wife's PPF account? Roshan Lal Shahi A: The funds received by the nominee of a bank account holder on the latters death is not taxable. The interest received on debentures issued by L&T Infrastructures would be taxable. The amount deposited by you in your wifes public provident fund account can be considered for the deduction allowable under Section 80C of the Income Tax Act. Q: I had a PPF account in the name of an Hindu undivided family, which was duly extended up to March 31, 2008. Due to some government notifications the account was not renewed further and hence with effect from April 1, 2008, the bank has not accepted any deposit in the account but still the interest on the balance was being levied. In May, 2012, I came to know that no interest was levied in the account from April 1, 2011 onwards. Bank officials did not provide any information regarding suspension of interest to me. I had withdrawn the balance amount Rs 28 lakh on May 5, 2012 on which no interest was levied from March 31, 2011 to May 5. The levy of interest was suddenly stopped without informing me. To whom should I complain to claim the specific interest amount? S.K. Jindal A: The PPF Scheme of 1968 was amended in Dec 2010, whereby an account opened under the scheme on behalf of a HUF was required to be closed after the expiry of 15 years from the end of the year in which the initial subscription was made and, if that period had expired, the account would be closed by March 31, 2011. The entire amount standing to be credited of the subscriber was required to be refunded after the said date. The bank should have informed you about the amendment and refunded the said amount to you. You may take up the matter with the consumer court.

|

||

|

personal

finance

Offers aimed at retail investors

Concerns The RGESS scheme may open a window of opportunities for retail investors; however, it has raised many eyebrows in terms of its success in future.

Conclusion The government has made an honest effort to revive equity participation in India by introducing RGESS, but the very complex nature of transactions and the costly maintenance of a demat account may not encourage first-time investors. Also, the meager tax rebate may not excite investors to take so much pain; however, the market will wait for detailed guidelines for the scheme from SEBI for more clarity. Rightly said, in the Rajiv Gandhi Equity Savings Scheme (RGESS), beauty is only skin deep. The author is associate VP (research & advisory - third party products) at Motilal Oswal Private Wealth Management. The views expressed in this article are his own

|

||

|

Taking a home loan from a different city

Is it really difficult to get a home loan even when you are eligible for it and have a good credit score? But what in case you want to buy a property in some city other than where you currently reside? It is not even in the context of a common single market where many foreign direct investors will testify that this is not just a rhetorical question. In fact the early investors in the India story discovered the maze of local taxes, levies and regulations divided India into many small markets (of which some were more profitably serviceable from manufacturing locations located outside India rather than from a location within India). Anyway, much water has flown down the Ganges since those early days and the impending implementation of the goods & services tax would perhaps be the culmination of a series of steps that have already been initiated in recent years to forge a common Indian market. The question is in the relatively mundane context of home loans. Recently I spoke to a friend of mine who wanted to a buy a flat in Kolkata while he was working in Mumbai. He wanted to use my expertise on home loan to suggest solutions for a problem that he was facing in getting a loan. He approached a bank in Kolkata which said it would have given him the loan as both the property and his income papers were in order, but it had asked him to visit its branch in Mumbai to get a loan as he was working in that city. When we came back to Mumbai after finalizing the property deal in Kolkata, he approached the branch of the same bank only to be informed to visit a branch in Kolkata as the property is located there and the bank wanted to value the property before giving the loan. This friend of mine had already paid Rs 51,000 for the booking amount. If he was unable to book the flat, the developer would return back only 50% of the booking amount (after negotiations as the developer was not ready to return a penny out of it). Having becoming tense over all these issues, he called me up and asked: "Is India really one nation?" The property was ready to move into with all the title documents and his loan eligibility was coming to more than Rs 20 lakh (though he required only Rs 14 lakh). I decided to do some research on the matter as the number of people moving to other cities for work has been increasing significantly. This may be a common problem faced by quite a few of them who either have plans of relocating or to buy a property for their parents in their home city. We did a round of mystery shopping as well as spoke to the major home loan players. Here is what we found - when we spoke to the players officially each of the players said that such loans are no problems as they have a single common system across the country. However the situation on the ground was a little different. From among the lenders we spoke to as mystery shoppers only two private lenders followed up on our initial call (we had dangled the bait of Rs 70 lakh home loan). Even the official we spoke to in a PSU bank assured us that they would be able to do the transaction subject to their normal credit and operational checks. The other two private sector banks and the one foreign bank that we spoke to as mystery customers either told us that they could not do such a deal or did not respond back after taking down the initial details. We already knew a few direct sales associates and thought of getting this answered from them also. We spoke to a large number of DSAs based out of Mumbai who serviced many banks. His feedback corroborated our own findings on mystery shopping. Another DSA we spoke to in Mumbai (who did not work with either of the private sector lenders) said he would be able to get the transaction done provided the project in Kolkata was pre-approved by any of the banks he worked for. I also did a bit of informal talking with the private sector banks that had turned down (or did not show much interest in) our mystery shopper. What came out was that none of them had an effective loan origination system across the country and unless the loan amount was big enough the amount of effort required to co-ordinate with another city was just not justified. Each office is driven by its own KRA (key result area) and as legal checking work done for another office was not counted as part of their KRAs this clearly did not enjoy any priority. What it boiled down to was that a loan that was clearly falling within their credit and legal norms of the bank was being given up simply because of the mismatch of KRAs between the two branch offices. Of course for a determined customer this would still be possible but it might take a lot more time than usual. The only saving grace to come out of this story was that at least for a few lenders India was a single country. The author is CEO of ApnaPaisa.com. The views expressed in this article are his own

|

||

|

| HOME PAGE | |

Punjab | Haryana | Jammu & Kashmir |

Himachal Pradesh | Regional Briefs |

Nation | Opinions | | Business | Sports | World | Letters | Chandigarh | Ludhiana | Delhi | | Calendar | Weather | Archive | Subscribe | E-mail | |

Equity runs but derails too. The global equity markets have been bleeding for quite a long time, so with India as the principle of decoupling has gone for a toss. India is a country of negligible financial literacy and investors still prefer traditional investment products like fixed deposits, post office savings schemes, etc. Amid low equity participation and continuous outflows in equity mutual funds post ban of entry load, the government announced a series of reforms including the widely awaited Rajiv Gandhi Equity Savings Scheme (RGESS), a mention in the FY2012-13 financial budget presented earlier this year. The scheme aims to increase penetration of investment into equities and improve the depth of Indian capital market as claimed by the government. But can tax incentives alone lure investors into this scheme?

Equity runs but derails too. The global equity markets have been bleeding for quite a long time, so with India as the principle of decoupling has gone for a toss. India is a country of negligible financial literacy and investors still prefer traditional investment products like fixed deposits, post office savings schemes, etc. Amid low equity participation and continuous outflows in equity mutual funds post ban of entry load, the government announced a series of reforms including the widely awaited Rajiv Gandhi Equity Savings Scheme (RGESS), a mention in the FY2012-13 financial budget presented earlier this year. The scheme aims to increase penetration of investment into equities and improve the depth of Indian capital market as claimed by the government. But can tax incentives alone lure investors into this scheme?

There is a wind of change in the sugar industry and, for the first time in years, sugar production estimates have has been revised downwards. The Indian Sugar Mills Association (ISMA) is monitoring the situation closely. Sugar prices have to remain viable for the mills to pay remunerative cane price on time to farmers, so that they continue to remain interested in sugarcane in 2013-14. Therefore, there should not be any big hurry to import sugar. ISMA director general Abinash Verma in an interview with Girja Shankar Kaura talks about the prospects of the sugar industry in the coming years.

There is a wind of change in the sugar industry and, for the first time in years, sugar production estimates have has been revised downwards. The Indian Sugar Mills Association (ISMA) is monitoring the situation closely. Sugar prices have to remain viable for the mills to pay remunerative cane price on time to farmers, so that they continue to remain interested in sugarcane in 2013-14. Therefore, there should not be any big hurry to import sugar. ISMA director general Abinash Verma in an interview with Girja Shankar Kaura talks about the prospects of the sugar industry in the coming years.

A: Though the cultivated area under sugarcane in the country has increased by 5 per cent over 2011-12, cane availability in Maharashtra and Karnataka will be lower due to deficient monsoon. The cane acreage is marginally lower for these states and some raw cane products have also been converted into fodder. However, cane area in Uttar Pradesh is at its highest ever and, therefore, production from Uttar Pradesh will partly compensate for the fall in the sugar production from Maharashtra and Karnataka. Considering these factors, we estimate sugar production of 2.4 million tonnes for the next year. For the second time, ISMA and National Federation of Cooperative Sugar Factories Ltd (NFCSF) have jointly carried out its satellite mapping exercise. Our estimations for 2011-12 were right on target. With the support of this technology and large number of field visits, combined with some tactful analysis of historical data, we feel that our estimations will be hold good.

A: Though the cultivated area under sugarcane in the country has increased by 5 per cent over 2011-12, cane availability in Maharashtra and Karnataka will be lower due to deficient monsoon. The cane acreage is marginally lower for these states and some raw cane products have also been converted into fodder. However, cane area in Uttar Pradesh is at its highest ever and, therefore, production from Uttar Pradesh will partly compensate for the fall in the sugar production from Maharashtra and Karnataka. Considering these factors, we estimate sugar production of 2.4 million tonnes for the next year. For the second time, ISMA and National Federation of Cooperative Sugar Factories Ltd (NFCSF) have jointly carried out its satellite mapping exercise. Our estimations for 2011-12 were right on target. With the support of this technology and large number of field visits, combined with some tactful analysis of historical data, we feel that our estimations will be hold good. Equity runs but derails too. The global equity markets have been bleeding for quite a long time, so with India as the principle of decoupling has gone for a toss. India is a country of negligible financial literacy and investors still prefer traditional investment products like fixed deposits, post office savings schemes, etc. Amid low equity participation and continuous outflows in equity mutual funds post ban of entry load, the government announced a series of reforms including the widely awaited Rajiv Gandhi Equity Savings Scheme (RGESS), a mention in the FY2012-13 financial budget presented earlier this year. The scheme aims to increase penetration of investment into equities and improve the depth of Indian capital market as claimed by the government. But can tax incentives alone lure investors into this scheme?

Equity runs but derails too. The global equity markets have been bleeding for quite a long time, so with India as the principle of decoupling has gone for a toss. India is a country of negligible financial literacy and investors still prefer traditional investment products like fixed deposits, post office savings schemes, etc. Amid low equity participation and continuous outflows in equity mutual funds post ban of entry load, the government announced a series of reforms including the widely awaited Rajiv Gandhi Equity Savings Scheme (RGESS), a mention in the FY2012-13 financial budget presented earlier this year. The scheme aims to increase penetration of investment into equities and improve the depth of Indian capital market as claimed by the government. But can tax incentives alone lure investors into this scheme?