|

|

|

|

|

Essentials of financial planning for women

Getting the best deal on your home loan

|

|

||||||||||||||||||||||||||||||||||||||||||||||

|

|

investor guidance No inheritance tax applicable in India My sister was allotted a society flat in Delhi in 1998. She bequeathed it to me in her will as part of her immoveable properties.

|

|

Essentials of financial planning for women

A recent study conducted last year by a financial institution revealed that in urban India only 13% of urban women are confident about the adequacy of their financial plans. Other startling figures show that 42% of educated urban women have only a basic plan in place that falls short of covering all long-term goals. In this age of gender equality, where financial security is the key to independence, these facts come as an unpleasant revelation.

There are several sociological reasons behind a womens reluctance to take up financial planning. For starters, there is a general perception that money and money matters are mens domain and women are best kept away from it. There is also a slight hesitation that creeps in when women are surrounded by financial jargon leading them to disengage from the conversation. Its high time these perceptions are shattered. There is an equal need for a man and a woman for financial planning. In fact, a womens financial situation is unique. While a mans financial aim is wealth accumulation, women tend to focus on the financial security of their children and themselves. Besides financial goals, a womans money-related needs are different from that of a man. For example, a womens genetic and biological makeup makes her vulnerable to specific medical and health situations causing financial drain. Then there is the weight of our social make-up where events like a pregnancy comes with its own share of financial changes. It isnt uncommon to see women opting out of career and settling down for low-paying jobs to balance career and motherhood. Its also often seen that mothers often take prolonged leave of absence from their careers to take care of kids or ageing parents that may deplete their income source. All these factors dissuade sound financial planning for women who, in actuality need a larger corpus than men because of their higher life expectancy and shorter career span. Saving systematically comes naturally to women which enables them to build up an appropriate fund as long as they have a disciplined approach towards it. By following a series of steps towards financial planning, women can build an asset that will make them self-reliant and independent. Have a plan

Build a financial plan but listing your incomes and expenses and also putting in place your expected income in the future is important. This will help you chalk out your financial objectives. Factors like time, risk appetite and liabilities also play a key role while shaping the financial plan. Also, it is said financial planning must start with the beginning of financial year because it is very tough to catch time as you lag behind. Knowing your assets and liabilities early always pays you as you can pay off your debts early and build on your assets. Women must pay off their costly and expensive debts first after studying financial records. Choose your investment instrument

Choosing the right financial instrument is the key to success for your financial plan. If wealth creation is your goal, then you can use instruments like equity, MFs, ULIPs, pension plans or debt instruments such as bonds, G- Secs and PPF. If you need financial protection, then go for life or health insurance plans. Investing in ELSS, PPF and tax-saving bonds will help you reduce your tax burden. The great thing about financial planning is that a woman has several investment avenues to choose from. At any stage, an asset allocation approach is the ideal way to invest since a well-constructed and diversified portfolio reduces risks and ensures smooth returns. Women should also look at building a contingency fund so that savings can continue even in case of unforeseen circumstances like illness, death of spouse or loss of job. Because women are more likely to have work disruptions for care giving, they need to capitalise on savings opportunities while they are working, in order to compensate for a longer average longevity. Tax planning

This is another aspect of efficient financial planning. Saving tax acts as a double sword as it helps to reduce tax outgo and saved tax can be utilised in order to pay debts. Moreover, investments done under Section 80C such as life insurance and health insurance also provide risk cover and products like ULIPs help to grow your wealth. Tax planning must not be postponed to the end which is usually the case for an individual which results in hasty investment decisions just to save tax. Further, wrong investments dont generate returns corresponding to your financial goals and an individual generally end up at the wrong side. Be disciplined

Sound financial planning is completely dependent on discipline. Luckily, living in the day and age of technology, managing your finances are easy and can be done online or with the help of a financial adviser. While you stay disciplined to your investments, make sure you take the time to understand the nature and associated risk of each investment instrument before investing. Review investments

Reviewing your investments periodically is an important step to ensure that you stay on the financial course you chalked out for yourself. Review your investment in line with increased income or expense, new assets or liability acquisitions or changing market conditions. Finally, as the milestone you have been saving for approaches near, you would need to redeem your investments. At this junction, it would become important to sit down with your financial consultant and understand if there is any taxation issue involved with the redemption of your investments.

The author is CEO & co-founder, Policybazaar.com. The views expressed in this article are his own |

|

|

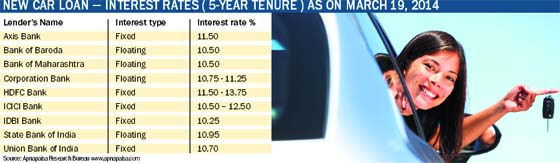

Getting the best deal on your home loan

Often buying a home is the largest purchase we make in our lifetime and taking a home loan to finance it, is likely to be the largest debt. Hence, it is essential to get the best deal to finance your home.

In a competitive market scenario, the financial institutions offer more and more consumer-friendly loan options. But, with so many product offerings available in the market with different features and varying interest rates, it is sometimes not easy to choose the right loan for your requirement. A little knowledge about home loan and what is being currently offered in the market will go a long way in getting the best deal on your home loan. But before you proceed to meet the lender, you need to ask few quick questions to yourself first. Some of the key questions are: What is the maximum loan amount I can avail? Normally, lenders finance maximum up to 80 to 90% of the agreement value (excluding stamp duty and registration charges) of the property. The final loan amount is dependent on a host of other factors like income and regular outgoings, repayment track record, valuation of the property by the lender, etc. Normally, the lender will assume around 40-45% of your net salary as available for payment of EMI to serve all the loans, though it varies from lender to lender and there is no standard norm/formula. Hence, your existing loans (if any) will also have an impact on your loan eligibility and the lender will calculate the eligibility based on the existing outstanding amount and the EMI being paid at the time of loan application. To increase the eligibility amount, you can add the earnings of your parents/spouse/ children and in some cases brothers as co-borrowers to the loan. Should I opt for fixed or floating rate home loan? Very few lenders offer pure fixed interest rate that remains fixed for the entire duration of loan. Some lenders do offer semi-fixed (also known as dual rate) where the interest rate remains fixed for duration 1-5 years and then gets converted to floating rate of interest. In floating rate, the interest rate fluctuates with market conditions. The rate of interest is tied up with the Base Rate (BR) of the bank or Prime Lending Rate (PLR) of the housing finance companies and gets affected whenever there are changes in the repo rates announced by RBI or any changes in Base Rate/PLR of the lender. Since a home loan is taken for a reasonably longer period, it is advisable to opt for floating rate of interest and not for fixed rate interest loan unless you feel that the rates of interest are at the lowest in the interest cycle. What is spread? Normally, the interest rate is calculated with reference to Base Rate or Prime Lending Rate. In case of base rate, it is expressed on the spread above base rate and in case of prime lending rate, it is normally expressed as spread below the PLR. It is a known fact that lenders are hesitant to reduce Base Rate & PLR when interest rates fall and hence consumer rarely get benefit of fall in market interest rates as quickly as they should get. The lender tends to provide the benefit of lower rates selectively to new borrowers by changing the spread rather than by decreasing the Base Rate/PLR. Therefore, you should ideally consider the spread (preferably lowest or nil in case of banks and highest in case of housing finance companies) along with the BR/PLR, if you want to get the benefit of lower interest rate on par with new customers. What tenure should I choose for my home loan? Most lenders offer maximum tenure of 30 years but it is also restricted by the borrowers age at the end of the tenure so as to ensure that the loan repayment ends on or before the retirement age of the borrower. Ideally, you should opt for a longer tenure floating rate loan to retain the flexibility of low EMIs and at the same time you can pre-pay the loan without any penalty whenever you have surplus funds. There are no additional costs involved if you opt for longer tenure. The interest that you pay will depend on the time for which you actually use the money. What are the charges I will have to bear for a home loan? Every loan has costs attached to it, some of which your lenders representative may fail to disclose during your loan application process. Get an estimate of all charges you may have to pay on your home loan, i.e. processing fee or administrative fee which are non- refundable, legal fee payable to the lender or to legal consultants of the lender, stamp duty on creation of mortgage, etc. The home loan offering continues to evolve and it is important you as a prospective borrower do your own research or talk to relevant adviser. You can also take help of online price and feature comparison engines to compare the latest interest rates, features, fee, etc. to shortlist the lenders. You should ideally shortlist four or five lenders and get the short-listed lenders to compete for your loan. The cost of your loan depends a lot on your ability to negotiate. Remember that all terms and conditions of a housing loan are negotiable if you have a good credit history.

The author is Product Manager, Apna Paisa. The views expressed in this article are his own |

|

|

No inheritance tax applicable in India

AN Shanbhag My sister was allotted a society flat in Delhi in 1998. She bequeathed it to me in her will as part of her immoveable properties. My queries are as under:

Sahil There is no inheritance tax applicable in India. You can most certainly will it to your son since now you are the legal owner of the property. You may also gift the property to your son. Gifting property to a close relative (you and your son are close relatives) does not attract any income tax. While transferring the flat in the name of the donee, stamp duty will have to be paid and this is usually much less than the normal. I am employed and living in a rented accommodation at the place of work for which I am paying Rs 12,000 pm. On the other hand, I have a home loan for the purchase of a house in the city where my parents reside. To claim the benefit of HRA and interest on home loan simultaneously whether it is compulsory to produce the rent note or the receipts of rent payment before the employer? Pratiyash Since you are not living in your own house and also actually paying rent, you are eligible for the exemption of HRA depending on your salary, HRA and rent paid. CBDT Circular 781 dt 5.11.99 exempts salaried employees drawing HRA up to Rs 3,000 per month from production of rent receipt. This concession is only for the purpose of administrative convenience of the employer while applying TDS. The claiming of deduction for housing loans is not connected with HRA. You have not mentioned in the query your salary per month. In any case, production of rent receipts would be required. I have some queries regarding buyback of shares.

Behal The option of 10% or 20% is not available in the case of property. This facility is only for shares, debt-based MF schemes and securities. Also, the tax rate is either 10% without indexation of cost or 20% after indexation of cost. You cannot pay 10% after indexation, irrespective of your tax slab. The STCG earned by selling shares (with STT paid) is taxable @15%. This does not change even if you pay the tax within 12 months etc. However, note that if your income, including the STCG is below the tax threshold applicable to you, the STCG will be tax-free. My father passed away in November 2013. He had some bank fixed deposits for which I was a nominee. My queries are:

Gurwinder Singh The best way of handling this situation is to file two tax returns for your father: i) In the name of your father till the date of his death and

|

|

| HOME PAGE | |

Punjab | Haryana | Jammu & Kashmir |

Himachal Pradesh | Regional Briefs |

Nation | Opinions | | Business | Sports | World | Letters | Chandigarh | Ludhiana | Delhi | | Calendar | Weather | Archive | Subscribe | E-mail | |

A recent study conducted last year by a financial institution revealed that in urban India only 13% of urban women are confident about the adequacy of their financial plans. Other startling figures show that 42% of educated urban women have only a basic plan in place that falls short of covering all long-term goals.

A recent study conducted last year by a financial institution revealed that in urban India only 13% of urban women are confident about the adequacy of their financial plans. Other startling figures show that 42% of educated urban women have only a basic plan in place that falls short of covering all long-term goals.

Often buying a home is the largest purchase we make in our lifetime and taking a home loan to finance it, is likely to be the largest debt. Hence, it is essential to get the best deal to finance your home.

Often buying a home is the largest purchase we make in our lifetime and taking a home loan to finance it, is likely to be the largest debt. Hence, it is essential to get the best deal to finance your home.