|

|

|

|

|

Economy

All eyes on the new FM |

|

|

|

|

Whats the new dawn that business wants By Sanjeev Sharma The business sentiment following the formation of Modi sarkar is upbeat. The fundamentals of the economy may not change immediately but the atmospherics have changed for the better. The Tribune takes a look at the gap between what the business expects and the limitations of the government.

As evidence of the uplift in sentiment, stock markets are at an all-time high, the rupee is around 59 to the dollar, foreign inflows have become more robust, corporate deals have become more active and most analysts are now talking of higher growth rates for the economy in the next five years. A recent Ficci survey showed that a whopping 93 per cent of CEOs polled expected a substantial improvement in the near term economic situation with a new government coming at the helm. Business sentiment is often an abstract and difficult to describe variable and is hard to pin down as to what will alter it for the better or worse. In Indias case, a fresh, strong mandate and a new pro-business and pro-reforms regime led by Modi seems to have done the job. However, the flip side of the enthusiasm in industry circles is that expectations are running high from the new dispensation. And given the fiscal constraints, analysts at Kotak Equities reckon that the government may not be in a position to provide a stimulus package or increase spending to revive demand. While various sectors have their own demands, there are pervasive demands like getting projects kick-started, expediting clearances, increasing the ease of doing business in India or reviving the business sentiment and investments, which cut across sectors and, therefore, impact the economy as a whole. Macro economySub-5% growth for two straight years

"India needs a chief executive officer as a Prime Minister that Modi represents," says Bundeep Singh Rangar, chairman of London-based consulting firm IndusView. Capital investment contributes nearly 35 per cent to India's $1.8 trillion economy, but it barely grew in the fiscal year that ended in March as delays in clearances from various ministries and funding issues grounded many major projects. India's current tax base represents fewer than 35 million, or a dismal 3 per cent of its population. Contrast it with the size of its middle class estimated to be 250 million people, expected to reach 600 million by 2030. Rating agency ICRA notes that some of the critical challenges that would need to be addressed are a consistent roadmap for fiscal consolidation, with clarity on issues such as tax reform, disinvestment and expenditure rationalisation, to free up fiscal space for development and infrastructure spending. In addition, it advocates a balanced approach to agriculture sector policies to ensure food security and tackle persistent food inflation. It has also stressed on clarity on energy reforms, which would encompass the whole gamut of areas, including auction of coal blocks, natural gas pricing and distribution reforms. InfrastructureGet stalled projects moving

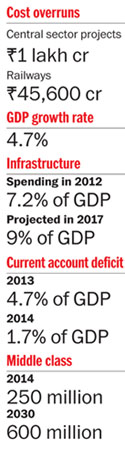

According to the latest report by AT Kearney, infrastructure spending is expected to grow from 7.2 per cent of the GDP in 2012 to 9 per cent by 2017. Road equipment is one of the segments that has seen considerable growth in the past few years. For the current financial year, the NHAI plans to award 2,000 km through cash contracts, and is ready with 3,000 km to be bid via the public-private partnership mode. With a strong pipeline of road projects to be awarded by the NHAI and state governments, the opportunities for road equipment manufacturers are sizeable. N Sivaraman, president, L&T Finance Holdings, feels the economy faces challenges like delay in projects sanctioning, inadequate government funding and diminishing projects in the infrastructure and mining sectors. He says corporates are also facing liquidity crunch and their funds have remained locked up, causing failure in loan repayment. The government should bring in stability, and only then will these problems be solved. According to an Assocham study, delays in the execution of central sector projects have resulted in cost overruns exceeding a whopping Rs 1 lakh crore, with the railways being on top of the list. In sectors like the railways, power and coal, there is no shortage of demand. The problem is of supply matching the demand even in an environment of slowdown," says Assocham president Rana Kapoor. Cost overruns due to delays in the execution of central projects are the maximum in the railways among infrastructure projects running into Rs 45,600 crore. At the end of March 2013, 41 railways projects with original cost estimates of Rs 27,900 crore saw an escalation of nearly Rs 73,500 crore. ExportsRising rupee not helping

The EEPC, an engineering exporters body, expects the government to initiate labour reforms and boost manufacturing. "We hope the government will be able to take some bold decisions regarding labour reforms which will benefit the Indian workforce and create new employment. We also expect a significant improvement in the quality of governance, that will in turn reduce transaction cost of Indian exporters and make them competitive in the world," EEPC chairman Anupam Shah says. Indian exports, with 45 per cent contributions from the MSME sector, have been languishing for the last few years. "We expect some key decisions from the new government in the coming foreign trade policy," he says. M Rafeeque Ahmed, president, Federation of Indian Export Organsiations, says the government will have to bring back manufacturing on track to sustain export and economy. Since Modi has already put his focus on five Ts, including trade and tourism both a big earner of foreign exchange he will devote greater attention to export as well. The government has to address infrastructure bottlenecks to impart competitiveness to exports, he says. Indias current account deficit (CAD) narrowed sharply to $32.4 billion (1.7 per cent of GDP) in fiscal 2014 from $87.8 billion (4.7 per cent of GDP) in fiscal 2013. The correction in CAD was primarily due to a contraction in merchandise imports coupled with a rise in service exports. Manufacturing Enhance competitiveness

Harsh Pati Singhania, vice-chairman and MD, JK Paper, says the focus must be on improving Indian business competitiveness, especially in the manufacturing sector, and making India an easier place to do business in. P Balendran, vice-president, General Motors India, feels the customer sentiment is expected to improve in the medium to long term. "We expect excise duty cuts to be retained in Junes budget and interest rates to fall or remain at current levels for any chances of recovery for the automobile sector during the second half of the year," he says. The I¬¬ndia Electronics and Semiconductor Association seeks to make India a manufacturing and innovation centre for domestic and global players in the electronics industry. "We envisage encouragement to industry and focus on building fab units and electronic manufacturing clusters with an investment potential of over Rs 75,000 crore in short term and cumulatively employing 28 million people by building the local ecosystem within the next 10 years," says Ashok Chandak, chairman of the association. TaxationBig hopes from maiden budget

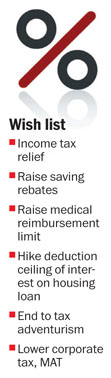

The PHD Chamber of Commerce and Industry has sought to raise the limit of medical reimbursement for salaried persona to a minimum level of Rs 50,000, as also hike the deduction ceiling of interest on housing loan to a minimum of Rs 5 lakh per annum, besides raising the present income tax limit for taxation purpose to Rs 2.5 lakh per annum. In a presentation to the Finance Ministry, the chamber said the limit for medical reimbursements for a vast majority of working class stand at Rs 15,000 per annum under Section 17 of the Income Tax Act for years and now needs to be revised at Rs 50,000 in view of persistently rising inflation and high cost of medical expenses. Similarly, the ceiling of interest on housing loan has not been revised for quite sometime which stays at Rs 1.5 lakh per annum and now urgently needs to be reviewed, keeping in view the rising property prices followed by high rates of interest rates coupled with increasing inflationary pressures. According to the PHD Chamber, this limit should be raised at Rs 5 lakh per annum to enable a vast section of working class to excess property and raise dwelling units for themselves under the flagship programmes of various state governments such as "build and own your properties". It has urged the Finance Ministry to bring down the corporate tax and minimum alternate tax (MAT) to 25 per cent and 10 per cent from their current aggregate levels of 32.445 per cent and 18.50 per cent, respectively. On the larger tax reforms, Ficci has sought an end to tax adventurism, resolve retrospective/capital raising related tax issues, retrospective actions, if at all, must invariably favour the taxpayer and rebated income tax for small, start-up businesses linked to employment creation. Power Renewable sector needs thrust

Ratul Puri, chairman, Hindustan Powerprojects, says the proposed national energy policy should provide a road map on all key objectives such as maximising the potential of all resources oil, gas, hydro, solar, wind, nuclear, coal; promoting domestic coal, oil exploration and production to reduce the import bill; developing indigenous capacities to meet the emerging needs; and a thrust to renewable sector like solar and wind. On the renewable energy front, TERI says power generation from renewable sources is on the rise. The share of renewables in the total energy mix reached 12.3 per cent in the year 2013. TERI has recommended that "wind mission" should be launched in the country as early as possible. Solar energy is important and a comparatively underutilised energy resource, with the potential to supply both grid-connected and off-grid power. It proposes an integrated renewable energy policy to mainstream renewables; and a national renewable energy law for a larger role for renewables in the energy sector with emphasis on renewable power. Priority must be given to the allocation of land resources to renewable power projects. Ficci has called for resolving the coal and iron ore impasse; market-based fuel pricing; tackling subsidies to curtail oil import impacts; and moderate import dependence for natural resources and commodities. The Association of Power Producers has welcomed the announcement of portfolios, which brought power, coal and renewable energy ministries under a common Minister of State with independent charge. Bringing these ministries under a common leadership augurs well for the power sector as the move will enable cohesive functioning among these interrelated ministries and help address the key priorities in a seamless manner, it says. Real estate Prop sagging sector

He says the reforms should cover administrative, banking, tax and legal aspects. It is imperative to go for a single-window system of approvals, correct the RBIs perception of housing sector and a balanced land policy that will help the farmers as well as developers. Pradeep Jain, chairman, Parsvnath Developers, says that the sector will be given industry status this time, which will ease the fund inflow. "Hopefully the new government will take corrective measures to boost the foreign direct investment into the sector," he says. Gold/jewellerY The shine is off

Ficci president Sidharth Birla says this move will help in the reduction of gold prices in the domestic market and will also help in reviving the growth of industry slowly. For the last one year, the growth of the gems and jewellery sector has been negatively impacted due to various restrictions imposed on gold imports, says Mehul Choksi, chairman FICCI Luxury Lifestyle Gems and Jewellery Forum, and chairman, Gitanjali Groups. The policy restrictions imposed on this sector, which were intended to control the investment demand of gold, has negatively impacted the domestic jewellery production, employment and also exports. As per recent reports, gold jewellery exports from India fell 39.63 per cent to $7.86 billion in the year to March 2014. The curbs have also spurred smuggling into India, the world's biggest buyer of gold, through "hawala" channels, which are informal international networks for remitting money, he says. However, in the financial year 2015, CRISIL Research expects the current account deficit to widen to $47 billion (2.2 per cent of the Gross Domestic Product) as restrictions on gold imports are gradually withdrawn and imports of capital and consumption goods pick up following economic recovery. Banking Rate cuts once inflation down

The banking sector faces issues of burgeoning NPAs and financing of capital adequacy norms of banks. The sluggishness in the domestic growth during the recent past and the tepid recovery in the global economy have impacted the NPAs. Gross NPAs of PSBs have risen from 3.84 per cent as on March 2013 to 4.44 per cent as at the end of March 2014. The government indicated that it alone cannot finance the entire requirements of PSU banks and has also asked them to explore avenues. The Finance Ministry is considering a holding company structure for banks to raise resources for capital adequacy requirements.

Focus on small savings Rajesh Sud, CEO and MD, Max Life Insurance, says life insurance plays a critical role in the utilisation of small savings for infrastructure development. To help the sector further enhance this role, the government has to provide right tax savings support to the long-term savings instruments and clearly differentiate it from short-term financial instruments. He says an additional tax incentive of Rs 1.5 lakh to life insurance and Rs 1 lakh for retirement plans could result in significant growth in the life insurance industry, which will also result in additional inflow of Rs 90,000 crore in infrastructure and Rs 2,20,000 crore into government securities by financial year 2020. Opening up of FDI avenues should bring in further long-term capital and the government should implement the long pending Insurance Bill amendment, he adds. Services Make health national priority

Develop tourism initiatives

Suri says under the new government, they are expecting major pro-tourism initiatives. Also, the BJPs commitment to create 50 affordable tourism circuits will give a big boost to the domestic travel market, with travellers getting more options to explore new destinations within the country. A section of e-commerce players have sought FDI in the sector. Manmohan Agarwal, CEO, Yebhi.com, says: "The Indian e-commerce industry is in dire need of capital. India has the potential to become one of the largest markets for e-commerce. By restricting the entry of foreign capital, technology and expertise, the government is scuttling the growth of this industry." In the last three years, the industry has witnessed an incredible growth of 150 per cent, increasing from $3.8 billion (Rs 19,249 crore) in 2009 to $9.5 billion (Rs 47,349 crore) in 2012.

|

|

The new Finance Minister Arun Jaitley will be presenting the governments maiden Budget in the first week of July, at a time when expectations of the people from the huge mandate are running high.

For most part of the last two decades, North Block has seen five incumbents. Former Prime Minister Manmohan Singh, President Pranab Mukherjee and P Chidambaram were Finance Ministers during the UPA rule while Jaswant Singh and Yashwant Sinha held the portfolio during the previous NDA regime. During their stints, Mukherjee and Chidambaram have been No. 2 in the UPA government and the face of the administration. In his debut innings, Jaitley, who has been closely associated with the cricket administration, is sizing up the pitch he has to bat on. He has a huge task of turning around the economy which has clocked sub-5 per cent growth for two straight years. Just over a month-and-a-half of his taking charge, Jaitley will be presenting this governments maiden Budget in the first week of July. He has said his priorities would be to tackle inflation, boost economic growth and follow the path of fiscal consolidation, among others. While these are universally accepted goals, often the tricky part is to find a balance as pushing one objective tends to disturb the other variable. Jaitley has stressed on maintaining a balance between growth and inflation. Restarting the investment cycle and moving towards higher growth and employment generation are also high on his list. The Finance Minister has also emphasised that the government would like to address the problem of inflation through supply side measures, particularly in relation to food inflation. The RBI will draw comfort from this statement as it would give it more room to cut interest rates as there has been a strong argument in some quarters that food inflation is best targeted through supply side structural reforms rather than interest rates. Among the challenges, Jaitley recently wrote on his Facebook post that the state of the economy "stares at all of us" with sub-5 per cent growth. He also alluded to "a lot of unpaid bills", possibly referring to Rs 80,000 crore of fuel and food subsidies that have been rolled over from the quarter of 2013-14 to the current year. "Mining and quarrying sectors have gained a negative growth trend. The manufacturing sector has had an abysmal performance last year. The investment cycle has been disturbed. The negative sentiment has affected trade, hotels and transportation sectors which are posed for a slower growth compared to last year. As per the CSO estimates released in May, inflation continues to be rising, with April figure at 8.9 per cent. The slowdown in economic growth coupled with high inflationary pressure poses a challenge to the macro economic environment. Tax collections are at 10.1 per cent of the GDP compared to the initial budget estimates of 10.9 per cent," he wrote in his post. Jaitley cautions further on the consequences. "India can ill afford this trend. This has serious social consequences since slowdown comes with a decade of jobless growth". On his future strategy, the Finance Minister emphasised that there is a need to boost domestic low-cost manufacturing and hasten the pace of reforms. Price stability and growth are inter-twined but may require a different strategy, he said. Referring to the mandate given by the people to this government, Jaitley added: "There was hope in the BJP/NDA led by Narendra Modi. It is this hope which commands us to pull the country out of the present economic situation. This will involve fiscal rectitude as combination of monetary and fiscal policy. Slower GDP growth will imply lower tax buoyancy and higher fiscal deficit. We must move towards an era of fiscal discipline where we can reduce the fiscal deficit, contain inflation and improve upon our growth rates." Jaitley seems to indicate that the country must prepare for tightening its belt, at least in the short term, as fiscal discipline will lead to tighter spending by the government. He is hoping that short-term discipline will lead to long-term benefits when growth picks up. "India must prepare itself for this. We must commit ourselves to this discipline in order to strengthen the Indian economy which can improve the quality of life of every Indian and pull out the deprived ones from the state of poverty. Short-term disciplining till we reverse the present trend will give us long-term benefits," he added. Sanjeev Sharma

|

|

| HOME PAGE | |

Punjab | Haryana | Jammu & Kashmir |

Himachal Pradesh | Regional Briefs |

Nation | Opinions | | Business | Sports | World | Letters | Chandigarh | Ludhiana | Delhi | | Calendar | Weather | Archive | Subscribe | Suggestion | E-mail | |

There

There

The

economy is in a weak spot with the GDP growth rate for 2013-14 at 4.7

per cent, below the official estimate of 4.9 per cent. This means that

India has now gone through two straight years of sub-5 per cent growth,

the worst showing in 25 years. Revival of growth in the economy remains

industrys biggest concern.

The

economy is in a weak spot with the GDP growth rate for 2013-14 at 4.7

per cent, below the official estimate of 4.9 per cent. This means that

India has now gone through two straight years of sub-5 per cent growth,

the worst showing in 25 years. Revival of growth in the economy remains

industrys biggest concern. The

sector is the key to growth and has remained bogged down in several

issues from land acquisition problems to slow clearances and perceived

viability of projects. The Indian Construction Equipment Manufacturers

Association says the government will have to unleash a wave of reforms

in multiple sectors, particularly in infrastructure, which forms the

backbone of the economy. The primary agenda is to

"de-bottleneck" stalled infrastructure projects on ground and

increase investments in the sector. "Infrastructure industry is

pinning hopes on the new government. However, I feel the road from

political stability to economic outcomes is rather a long one. The

government will have to work on some underlying issues to ensure long

term and sustainable progress," says Amit Gossain, the association

president.

The

sector is the key to growth and has remained bogged down in several

issues from land acquisition problems to slow clearances and perceived

viability of projects. The Indian Construction Equipment Manufacturers

Association says the government will have to unleash a wave of reforms

in multiple sectors, particularly in infrastructure, which forms the

backbone of the economy. The primary agenda is to

"de-bottleneck" stalled infrastructure projects on ground and

increase investments in the sector. "Infrastructure industry is

pinning hopes on the new government. However, I feel the road from

political stability to economic outcomes is rather a long one. The

government will have to work on some underlying issues to ensure long

term and sustainable progress," says Amit Gossain, the association

president. While

exports have picked up marginally due to improvement in the western

economies, the growth rate is much below the desired outcome. The

current account deficit has come down to 1.7 per cent of the GDP,

helping the macro situation, but the rising rupee is a worry for

exporters.

While

exports have picked up marginally due to improvement in the western

economies, the growth rate is much below the desired outcome. The

current account deficit has come down to 1.7 per cent of the GDP,

helping the macro situation, but the rising rupee is a worry for

exporters. It

has been the worst performing sector in the economy, growing only 0.4

per cent in the financial year 2014. This has also hurt job and capacity

creation and demand slump due to low confidence of consumers.

It

has been the worst performing sector in the economy, growing only 0.4

per cent in the financial year 2014. This has also hurt job and capacity

creation and demand slump due to low confidence of consumers. Given

that the middle class and salaried have voted heavily for Modi,

expectations of a cut in income tax relief are high. A study by Assocham

suggests that common taxpayers want relief from the maiden Budget.

Taxpayers want the new Finance Minister to provide for income tax

exemption threshold after factoring in inflation for the last five years

and raise the saving rebates beyond Rs 1 lakh as the incessant

double-digit retail inflation has eaten into household budgets through

an undeclared tax of price rise, says the study.

Given

that the middle class and salaried have voted heavily for Modi,

expectations of a cut in income tax relief are high. A study by Assocham

suggests that common taxpayers want relief from the maiden Budget.

Taxpayers want the new Finance Minister to provide for income tax

exemption threshold after factoring in inflation for the last five years

and raise the saving rebates beyond Rs 1 lakh as the incessant

double-digit retail inflation has eaten into household budgets through

an undeclared tax of price rise, says the study. This

sector has been struggling due to lack of coal linkages and problems

with the finances of state electricity board which are not able to pass

on the cost to the consumers.

This

sector has been struggling due to lack of coal linkages and problems

with the finances of state electricity board which are not able to pass

on the cost to the consumers. The

realty sector has been in the doldrums for a couple of years due to lack

of demand, weak economy and high interest rates. Realtors apex body

CREDAI chairman Lalit Kumar Jain hopes the Modi government will

immediately take up the much-needed realty reforms to boost the flagging

sector.

The

realty sector has been in the doldrums for a couple of years due to lack

of demand, weak economy and high interest rates. Realtors apex body

CREDAI chairman Lalit Kumar Jain hopes the Modi government will

immediately take up the much-needed realty reforms to boost the flagging

sector. The

precious metal has seen a huge shortage due to high duties and import

curbs to control the current account deficit. This has also led to

increased smuggling at airports. Recently the gold prices fell after the

RBI eased imports.

The

precious metal has seen a huge shortage due to high duties and import

curbs to control the current account deficit. This has also led to

increased smuggling at airports. Recently the gold prices fell after the

RBI eased imports. High

interest rates have been plaguing industry and consumers. The RBI has

indicated that once inflation is under control and the government does

its job on fiscal prudence, there will be room for rate cuts.

High

interest rates have been plaguing industry and consumers. The RBI has

indicated that once inflation is under control and the government does

its job on fiscal prudence, there will be room for rate cuts.

Fast

growing services which is taking up more and more of the economy as

sectors are opened has not maintained its momentum. Prathap C Reddy,

chairman, Apollo Hospitals Group, says health should be declared a

national priority as inclusive economic growth inherently demands a

first-rate healthcare system, one that is affordable and accessible. The

government needs to drastically increase public spending on health,

create a road map for universal health coverage, corporatise medical

education and take decisive steps to remove the barriers of

accessibility, cost and quality that continue to plague the healthcare

system, he says.

Fast

growing services which is taking up more and more of the economy as

sectors are opened has not maintained its momentum. Prathap C Reddy,

chairman, Apollo Hospitals Group, says health should be declared a

national priority as inclusive economic growth inherently demands a

first-rate healthcare system, one that is affordable and accessible. The

government needs to drastically increase public spending on health,

create a road map for universal health coverage, corporatise medical

education and take decisive steps to remove the barriers of

accessibility, cost and quality that continue to plague the healthcare

system, he says. Jyotsna

Suri, CMD, Lalit Suri Hospitality Group, says with the BJP identifying

tourism in its manifesto as a key sector to drive socio-economic

progress and one of the five pillars of Indias future growth, it

shows the new governments commitment to develop the tourism and

hospitality industry.

Jyotsna

Suri, CMD, Lalit Suri Hospitality Group, says with the BJP identifying

tourism in its manifesto as a key sector to drive socio-economic

progress and one of the five pillars of Indias future growth, it

shows the new governments commitment to develop the tourism and

hospitality industry. There

There